Most financial institutions have invested heavily in digital account opening. Consumers can open a checking or savings account or apply for a loan from their phone in minutes. But opening an account is only the beginning of the relationship.

The real challenge starts after the application is approved.

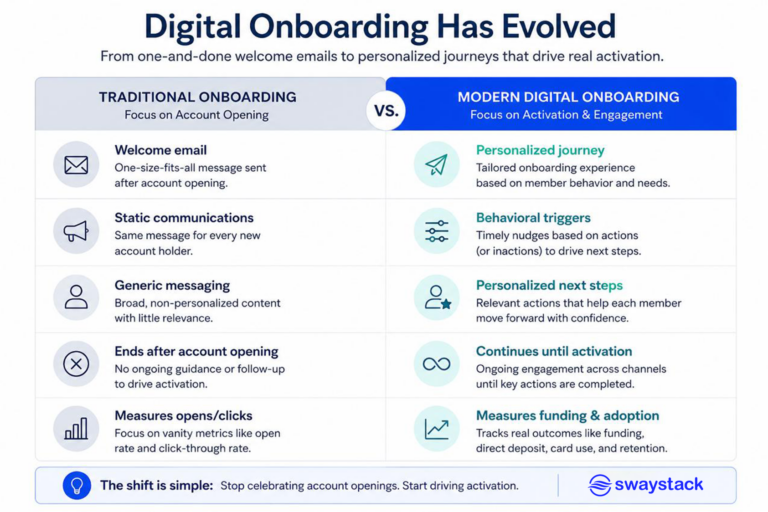

A new account that sits unfunded, lacks direct deposit, and never becomes the customer’s primary financial relationship delivering little long-term value. Yet many banks and credit unions still treat onboarding as a series of welcome emails rather than a strategic process designed to drive activation and engagement.

That’s why digital onboarding has become one of the most important growth opportunities in banking. Effective onboarding helps new account holders fund their accounts, enroll in digital banking, switch direct deposits, move recurring payments, adopt debit and credit cards, and discover additional products that fit their needs. The result is stronger customer relationships, higher retention, and greater lifetime value.

What Is Digital Onboarding in Banking?

Digital onboarding in banking is the process of guiding new users from account opening to active account usage. It encompasses every interaction that helps an account holder establish and deepen their relationship with a financial institution after becoming an account holder.

While digital account opening focuses on acquiring a new user, digital onboarding focuses on activating that account. The goal is to help account holders complete the actions that lead to long-term engagement and profitability.

Modern digital onboarding is typically delivered through online and mobile banking experiences, supported by personalized messaging, behavioral triggers, and guided workflows. Rather than relying on users to figure out the next steps on their own, effective onboarding solutions proactively help them complete key milestones.

The most successful institutions view onboarding as a journey rather than a one-time event. Instead of ending when an account is opened, the experience continues until account holders have fully adopted the products and services that create lasting value for both the user and the institution.

Why Digital Onboarding Matters More Than Ever

Consumer expectations have changed dramatically over the past decade. People now expect banking experiences to be as intuitive and guided as the digital experiences they encounter from leading technology companies. Opening an account online is no longer enough. Users expect clear next steps, personalized recommendations, and seamless tools that help them get value from their new account immediately.

At the same time, competition for primary financial relationships has intensified. Consumers often maintain accounts with multiple financial institutions, fintechs, and payment providers. Winning a new account does not guarantee that a bank or credit union will become the user’s primary banking provider. Without a deliberate onboarding strategy, many new accounts remain secondary relationships with limited activity and low profitability.

Perhaps most importantly, digital onboarding has become a critical differentiator in an increasingly digital-first banking environment. Institutions that provide a seamless path from account opening to active engagement create stronger user experiences and stronger financial outcomes. Those that do not risk losing attention, deposits, and long-term relationships to competitors that make activation easier.

For banks and credit unions focused on growth, digital onboarding is no longer a nice-to-have enhancement. It is a strategic capability that determines whether new accounts become active, profitable relationships, or simply another name in the core system.

Retail Digital Onboarding Best Practices

The most effective onboarding programs are designed around account activation. Rather than simply welcoming new account holders, they guide users through the actions that establish a primary banking relationship. The following best practices help banks and credit unions turn new accounts into engaged, long-term relationships.

1. Make Onboarding Part of Digital Banking

Many institutions treat onboarding as a separate experience delivered through email campaigns or standalone microsites. The problem is that users spend most of their time inside online and mobile banking, not in their inbox.

The best onboarding experiences are embedded directly within digital banking. When users log in, they should immediately see personalized next steps, progress indicators, and recommended actions based on their account status. This creates a seamless experience that meets account holders where they already manage their finances.

By integrating onboarding into digital banking, institutions can increase visibility, improve completion rates, and create a more consistent user experience.

2. Focus on Activation, Not Completion

Too many onboarding programs measure success by whether a user completed account opening. In reality, account opening is only the starting point.

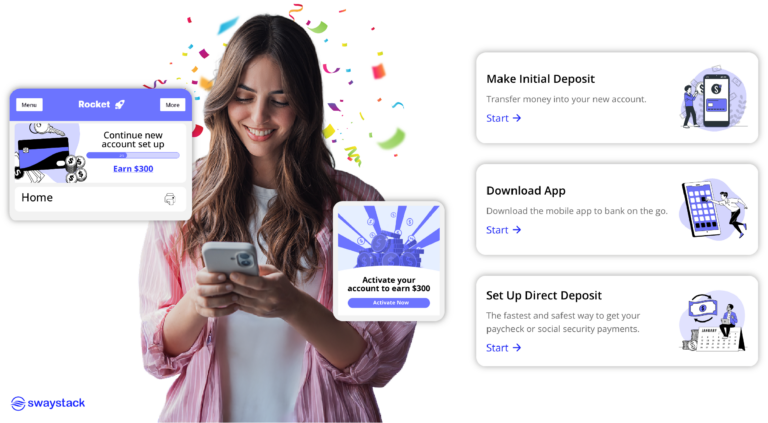

Effective onboarding focuses on activation metrics that indicate a user is building a meaningful relationship with the institution. These milestones may include funding the account, enrolling in digital banking, setting up direct deposit, making a debit card purchase, or establishing recurring transactions.

When onboarding is designed around activation outcomes rather than administrative completion, institutions can better align their efforts with long-term growth and profitability.

3. Drive Early Account Funding

An unfunded account is one of the strongest indicators that an account holder may never fully engage with the institution. That’s why encouraging initial deposits should be a top priority in onboarding.

The easier it is for users to move money into their new account, the more likely they are to begin using it as intended. Institutions should provide simple funding options, clear guidance, and timely reminders to encourage them to act quickly.

Early funding creates momentum. Once users have money in the account, they are significantly more likely to adopt additional services and make the institution part of their everyday financial life.

4. Win the Direct Deposit Relationship

Direct deposit remains one of the most powerful indicators of primary financial institution status. Account holders who route their paycheck into an account are more likely to maintain balances, use additional products, and remain loyal over time.

Unfortunately, many institutions leave users to navigate the direct deposit switching process on their own. Modern onboarding experiences simplify this step by providing guided workflows and digital tools that make switching fast and convenient.

Helping users establish direct deposit early in the relationship can dramatically improve activation rates and long-term account value.

5. Help Users Move Recurring Payments

Consumers often hesitate to switch financial institutions because of the effort required to update recurring payments and subscriptions. Streaming services, utilities, insurance providers, and countless other merchants may be tied to an existing account or card.

A strong onboarding experience removes this friction by helping account holders identify and transfer recurring payments to their new account. The easier it is to move these financial connections, the faster users can transition their daily banking activity.

Institutions that simplify payment migration reduce abandonment and increase the likelihood that users will make the new account their primary banking relationship.

6. Become the Card on File

Debit and credit card usage is another critical activation milestone. When an account holder’s card becomes the preferred payment method for everyday purchases, engagement naturally increases.

Onboarding programs should encourage card activation, first transactions, and card-on-file updates with key merchants. Educational prompts, reminders, and guided workflows can help users complete these actions without unnecessary friction.

The goal is not simply to issue a card but to make it the card that account holders reach for first.

7. Accelerate Digital Banking Adoption

Digital banking adoption is foundational to long-term engagement. Account holders who actively use online and mobile banking are more likely to interact with the institution, discover additional services, and remain connected over time.

Onboarding should guide users through key digital banking features, including mobile deposit, bill pay, account alerts, digital wallets, and financial management tools. Rather than overwhelming users with every feature at once, institutions should introduce capabilities gradually based on relevance and timing.

Helping users realize the value of digital banking early creates stronger engagement and a better overall experience.

8. Personalize the Journey and Follow-Up

Not every person has the same goals, behaviors, or financial needs. A one-size-fits-all onboarding experience often results in irrelevant messaging and missed opportunities.

Modern onboarding programs use user data and behavioral signals to personalize recommendations and next steps. A user who has already funded their account may need help setting up direct deposit, while another may need encouragement to enroll in mobile banking.

Personalization ensures that onboarding remains relevant, timely, and focused on the actions most likely to deepen the relationship.

9. Introduce the Next Product at the Right Time

Cross-selling should not begin the moment an account is opened. Account holders are more receptive to additional products after experiencing value in their initial relationship.

Effective onboarding identifies natural moments to introduce relevant products and services. An account holder who regularly maintains a balance may be a candidate for a savings account. Someone using a debit card frequently may benefit from a rewards credit card. A user receiving direct deposit may be interested in lending or financial wellness solutions.

By aligning product recommendations with user behavior and lifecycle stage, institutions can increase adoption while maintaining a customer-centric experience.

10. Use Gamification to Encourage Progress

The most successful onboarding experiences borrow engagement techniques from consumer apps. Gamification can motivate users to complete important onboarding milestones by making progress visible, rewarding achievement, and creating a sense of momentum.

Progress bars, onboarding checklists, milestone badges, and completion rewards can encourage account holders to take actions such as funding an account, enrolling in direct deposit, activating a card, or setting up digital banking features. Even simple visual indicators that show users how far they have progressed can significantly improve completion rates.

Common Digital Onboarding Mistakes

Even institutions that recognize the importance of onboarding often make mistakes that limit adoption and engagement. Avoiding these common pitfalls can significantly improve activation outcomes.

Relying on Welcome Emails Alone

Welcome emails can support onboarding, but they should not be the onboarding strategy. Users are far more likely to engage with guidance delivered directly within digital banking.

Measuring Activity Instead of Outcomes

Tracking email opens and login counts only tells part of the story. Focus on activation metrics such as account funding, direct deposit enrollment, card usage, and recurring payment adoption.

Treating Onboarding as a Marketing Project

Successful onboarding requires coordination across digital banking, operations, product, and marketing teams. It should be viewed as a growth strategy, not just a communications campaign.

Ending the Journey Too Early

Many onboarding programs stop after the first few days or weeks. In reality, account holders often need ongoing guidance before they fully adopt products and services.

Creating One Experience for Every User

Not all users have the same needs or goals. Generic onboarding journeys often miss opportunities to drive meaningful engagement through personalization.

The Future of Digital Onboarding in Banking

Digital onboarding is evolving from a fixed onboarding sequence into an intelligent, ongoing engagement strategy. As customer expectations continue to rise, financial institutions will increasingly rely on data, automation, and personalization to guide account holders toward deeper relationships.

AI-Driven Personalization

Artificial intelligence will enable onboarding experiences that adapt to each user’s behavior, goals, and financial needs. Rather than delivering the same journey to every user, institutions will be able to recommend the most relevant next steps, products, and services in real time.

Real-Time Behavioral Triggers

Future onboarding programs will respond immediately to user actions. Whether a user funds an account, activates a card, or enrolls in direct deposit, the next recommendation will be triggered automatically, creating a more relevant and timely experience.

Continuous Lifecycle Engagement

The line between onboarding and ongoing engagement will continue to blur. Instead of ending after the first few weeks, onboarding will evolve into a continuous journey that helps customers discover new features, adopt additional products, and achieve financial goals over time.

Embedded Financial Wellness Experiences

Financial wellness tools will become a more prominent part of onboarding. Budgeting guidance, savings recommendations, credit-building resources, and personalized insights can help account holders achieve better financial outcomes while strengthening their relationship with the institution.

Digital account opening may win the account, but digital onboarding wins the relationship.

Banks and credit unions that achieve the strongest growth outcomes understand that onboarding is not a one-time welcome campaign. It is a strategic process designed to help new account holders become active, engaged customers. By guiding users through critical milestones such as account funding, direct deposit setup, recurring payment transfers, card activation, and digital banking adoption, financial institutions can accelerate activation and increase long-term customer value.

As competition for primary financial relationships continues to intensify, effective onboarding will become an even more important differentiator. Users expect personalized guidance, seamless digital experiences, and clear next steps that help them get value from their accounts quickly. Institutions that deliver on those expectations will be better positioned to deepen relationships, improve retention, and drive sustainable growth.

The future of digital onboarding is not simply helping new users get started. It is creating a continuous engagement journey that turns new accounts into lasting relationships. For banks and credit unions looking to maximize the value of every new account, investing in a modern onboarding strategy is no longer optional—it is essential.

Ready to Improve Your Digital Onboarding?

The right onboarding strategy can increase funding, direct deposit adoption, card usage, and long-term engagement.

See how Swaystack helps banks and credit unions turn new accounts into active, primary relationships. Schedule a discovery call.

Digital onboarding is the process of guiding new customers after account opening to help them become active users. It includes actions such as account funding, direct deposit setup, digital banking enrollment, card activation, and product adoption.

Digital onboarding helps financial institutions turn new accounts into active relationships. Effective onboarding can increase account funding, direct deposit adoption, card usage, customer retention, and long-term profitability.

Digital account opening focuses on acquiring a new customer and creating the account. Digital onboarding begins after the account is opened and focuses on helping customers adopt products, engage with the institution, and establish a primary banking relationship.

Key onboarding metrics include account funding rates, direct deposit adoption, digital banking enrollment, debit card activation and usage, recurring payment transfers, product adoption, and account retention.

Modern digital onboarding solutions should include digital banking integration, account funding tools, direct deposit switching, personalized journeys, omnichannel engagement, real-time analytics, and automated next-best-action recommendations.

While the first 30 to 90 days are critical, onboarding should not end after a few weeks. The most effective institutions extend onboarding into an ongoing engagement strategy that helps customers discover new features, adopt additional products, and deepen their relationship over time.